2023/24 Year-end/New Year Travel Trend (Dec. 23, 2023, to Jan. 3, 2024)

JTB Corp.

●The number of Japanese domestic travelers is estimated at 28 million, representing 103.7% of the same figure a year earlier. Domestic travel expenditure is expected to reach record high.

●The number of outbound travelers is projected at 580,000, which represents 260.1% of the same figure a year earlier, making a significant recovery from a year ago.

●International travel is divided into long-term and short-term trips with travel expenditure polarized into low and high ends. Hawaii, South Korea, and Southeast Asia are popular destinations.

JTB compiled a report on a travel trend outlook for those who plan to go on an overnight or longer trips during the 2023/24 year-end/new year period (December 23-January 3). The report was prepared based on data such as economic indicators, industry trends, transport company activities, booking data of accommodation facilities, and opinion surveys. JTB began releasing the report in 1969, publishing the 54th report this year. No data on the average outbound travel expenditure and outbound travel spend was released for 2020 and 2021 when the border control measures were taken by the Japanese government for international departures and arrivals to combat the COVID-19 pandemic. The results of the recent survey are as follows.

(Figure 1) Estimated Number of Travelers and Expenditure for Year-end/New Year Trips

[Travel Trend Survey: Survey Method]

Survey period: November 13-16, 2023

Participants: Individuals aged 15-79 living in Japan

Number of samples: Preliminary survey 10,000; main survey 1,930

(The participants of the main survey were selected from those who had responded "Will travel" or "Will probably travel" during the 2023/24 year-end/new year period in the preliminary survey.)

Survey subject: Overnight or longer trips scheduled between December 23, 2023-January 4, 2024

(Domestic travel is limited to those for the purpose of sightseeing or hometown visits, while outbound travel includes business travel.)

Survey method: Online survey (Outsourced to: Macromill, Inc.)

*Because the survey results are rounded, there could be discrepancies in the sub-totals or differences with previous year's figures.

<Social and Economic Environment and Consumer Activities>

1.Receding of COVID-19 pandemic and current recovery status

The World Health Organization (WHO) announced in May 2023 the end of a global health emergency brought about by COVID-19, which had been affecting people's movements for more than three years. Following this announcement, in the same month, the Japanese authorities re-classified COVID-19 into Class-5, the same category as seasonal influenza, under the country's infectious disease laws. These brought people's lives mostly back to pre-COVID conditions.

The number of tourists has also been recovering steadily. The United Nations World Tourism Organization (UNWTO) announced that the number of international tourists worldwide during the January-July 2023 period had recovered to 84% of the same period in 2019. UNWTO predicts the number to recover to 80-95% of its pre-COVID level for the whole of 2023 and expects further growth in 2024. The situation, however, remains unpredictable given the continued rises in energy and other prices due to uncertain global conditions.

In Japan, the total number of domestic visitor nights in October 2023 (preliminary figure) was 41,333,000, representing 98.5% of the same figure in October 2022 (41,969,000 nights) when nationwide travel support measures were in force and 103.9% of the same figure in October 2019 (39,791,000 nights) before the COVID-19 pandemic*1. The number of inbound tourists to Japan in October 2023 (estimate) was 2,517,000, representing 504.7% of the same figure in October 2022 (499,000) and 100.8% of the same figure in October 2019 (2,497,000). This figure also exceeded its pre-COVID level*2. While tourism activities are returning nationwide, some tourist spots and areas are experiencing a service staff shortage and rising accommodation charges due to changes in the environment caused by the COVID-19 pandemic. In addition, there are concerns about overtourism.

*1: Source: A statistical survey of visitor nights by the Japan Tourism Agency; a preliminary figure for October 2023 and definitive figures for October 2019 and October 2022.

*2: Source: Numbers of inbound travelers to Japan and outbound Japanese travelers provided by the Japan National Tourism Organization (JNTO); an estimate for October 2023 and definitive figures for October 2019 and October 2022.

After the Japanese government ended its border control measures in April 2023, international travel has become easier in terms of national regulations. Recovery in outbound travelers, however, has been slow due to factors including inflations, the cheaper yen, and ongoing uncertainty in situations of certain areas. In October 2023, Japanese resident outbound departures stood at 938,000, representing 268.3% of October 2022 (350,000 departures). The October 2023 figure, however, only represents 56.4% of October 2019 (1,663,000 departures) *3.

*3: Source: Numbers of inbound travelers to Japan and Japanese resident outbound departures provided by the Japan National Tourism Organization (JNTO); an estimate for October 2023 and definitive figures for October 2019 and October 2022.

2.Economic environment and consumer sentiment concerning travel and leisure spending

Although the Japanese economy has been mostly freed from the restrictions placed on it by the COVID-19 pandemic, its economic outlook remains uncertain due to the impact of the deteriorating global situation, monetary policies in Europe and the United States, and other factors. The World Economic Outlook released by the International Monetary Fund (IMF) in October 2023 revised Japan's growth rate forecast upward but expected the 2024 growth rate to be below that of 2023. Furthermore, the Japanese government's monthly economic report released in November 2023 downgraded its assessment of Japan's basic economic conditions to "moderate recovery with standstill in some areas," although it maintained that personal consumption was "recovering" for seven months in a row. In addition to the risk of overseas economic downswings placing downward pressure on the Japanese economy, there are concerns about the impact of the rising inflation, Middle Eastern situation, and fluctuations in the financial and capital markets, among other factors.

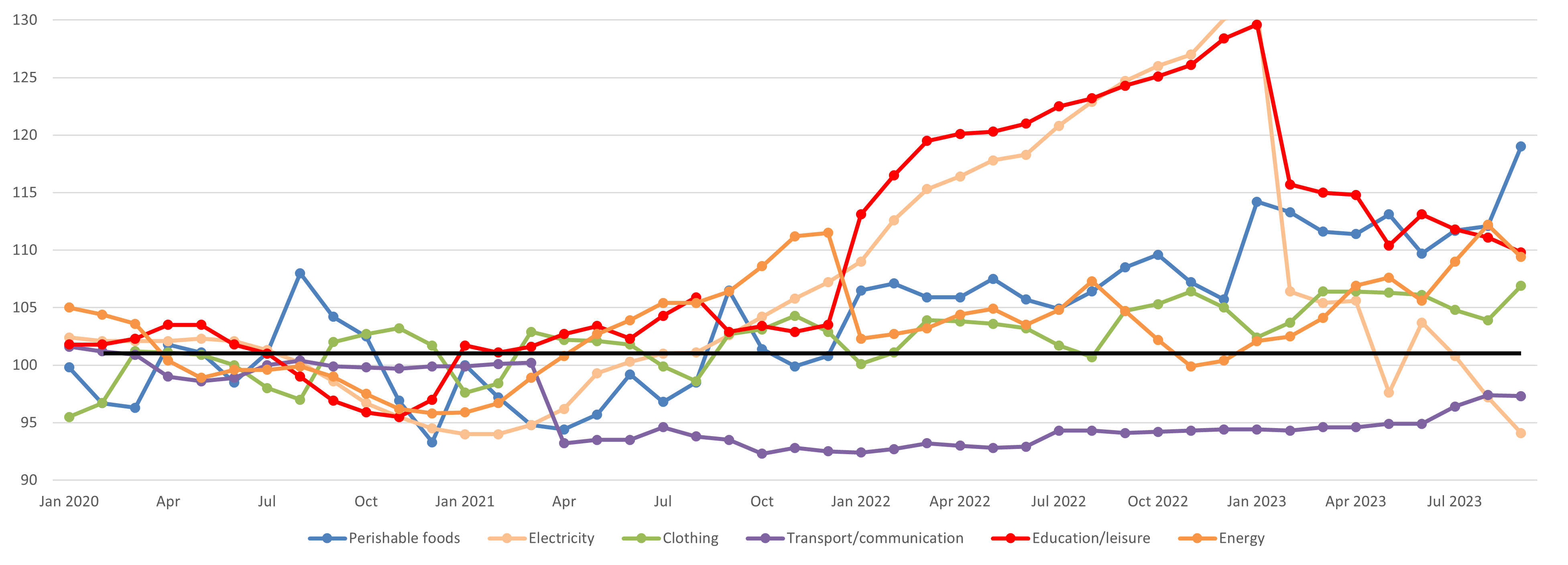

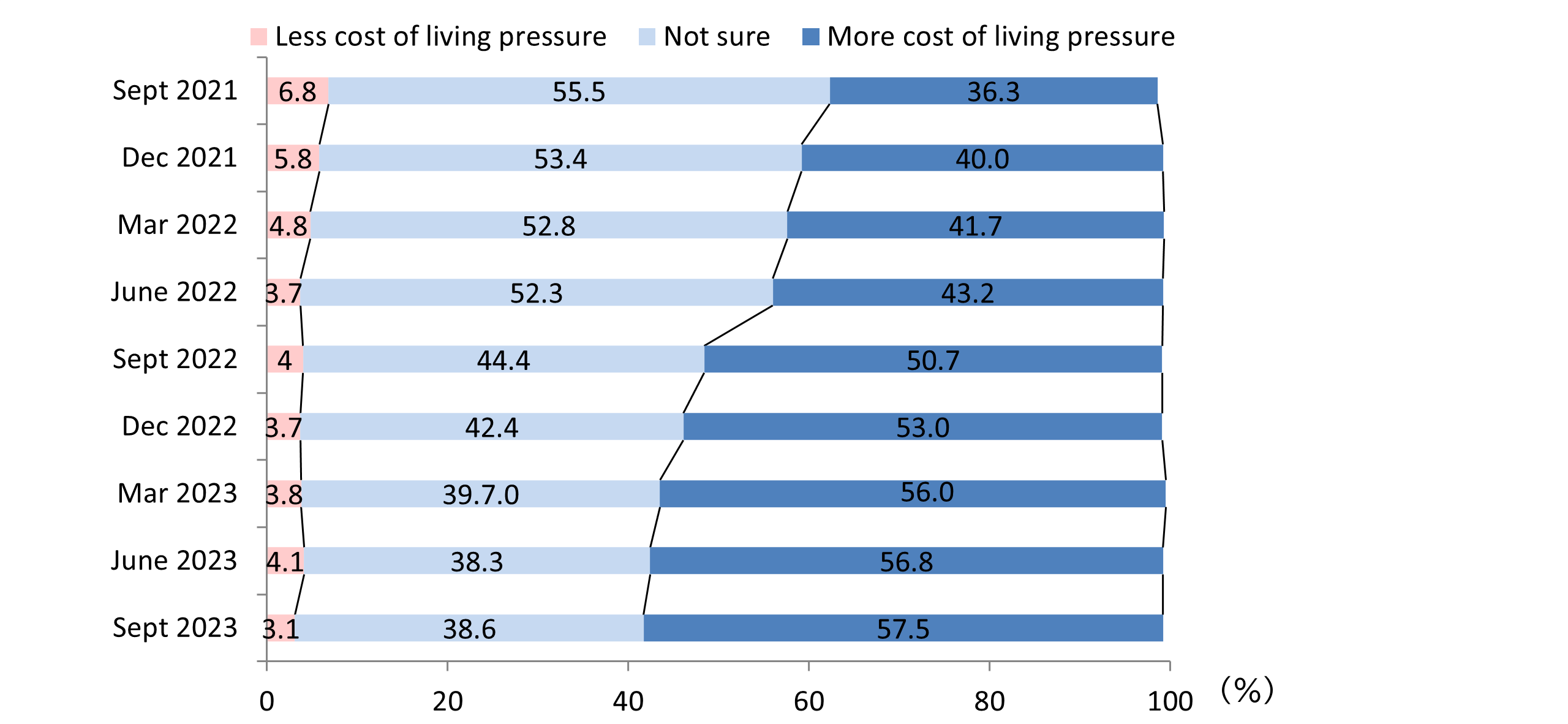

The Nikkei Stock Average continued exceeding ¥30,000, reaching a 33-year high on November 20, 2023. Meanwhile, current economic conditions remain difficult. On the FOREX market, the Japanese yen has rapidly depreciated against the US dollar since 2022, currently trading at around ¥150 to a dollar. The rising inflation since the second half of 2022 has also kept affecting households. Looking at the consumer price index of major items, while electricity cost has fallen compared with the previous year thanks to the subsidies provided by the Japanese government since January 2023, prices of essential items such as perishable foods, clothing, transport, and communication are still rising (Figure 2). The prices of regular unleaded gasoline recorded a 15-year high, exceeding ¥180/liter in August 2023. The prices have subsequently declined slightly due to the Japanese government's price control measures but are remaining at high levels. In this environment, the cost of living pressure is increasing. According to the current living conditions illustrated in a Bank of Japan survey on consumer sentiment, the ratio of respondents who are feeling a greater cost of living pressure has been consistently on the rise since September 2021, reaching 57.5% of all the respondents in September 2023, which is 17.5 percentage points (pp) higher compared with December 2021 (Figure 3).

(Figure 2) Consumer Price Index (CPI)

(Figure 3) Current Living Conditions

Source (Figure 2): Prepared by JTB Tourism Research & Consulting Co. based on consumer price index data (2020=100) provided by the Ministry of Internal Affairs and Communications, Japan

Source(Figure 3): Prepared by JTB Tourism Research & Consulting Co. based on data from the consumer sentiment surveys conducted by the Bank of Japan

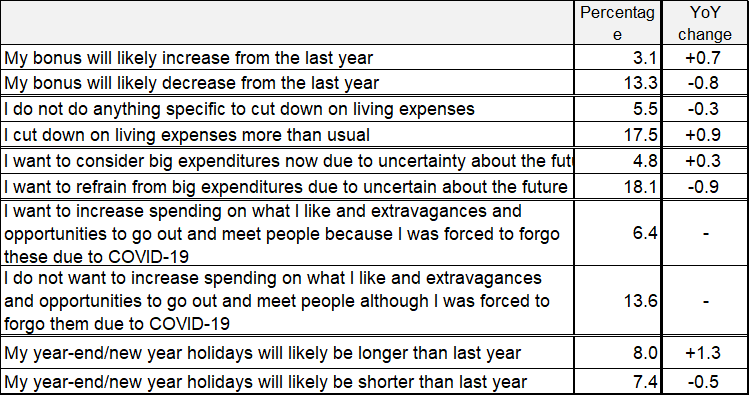

In its survey, JTB asked about the respondents' lives and plans for traveling during the 2023/24 year-end/new year period. Compared with the survey conducted a year earlier, the respondents who stated that their bonus was likely to increase from last year rose by 0.7 pp to 3.1% of all the respondents, while those stated that their bonus was likely to decrease from last year fell by 0.8 pp to 13.3%, indicating an improvement in terms of their income. Potentially due to these impacts, there were signs that the respondents were positive about big spending with a 0.3-pp increase in those responding to consider big spending now due to uncertainty about the future to 4.8% and a 0.9-pp fall in those responding to refrain from big spending due to uncertainty about the future to 18.1%. Meanwhile, with respect to the day-to-day cost of living, there was a 0.3-pp drop in those who were not doing anything specific to save their living expenses to 5.5% and a 0.9-pp rise in those who were cutting down on their living expenses more than usual to 17.5%. This shows that consumers are wanting to make more targeted spending (Figure 4).

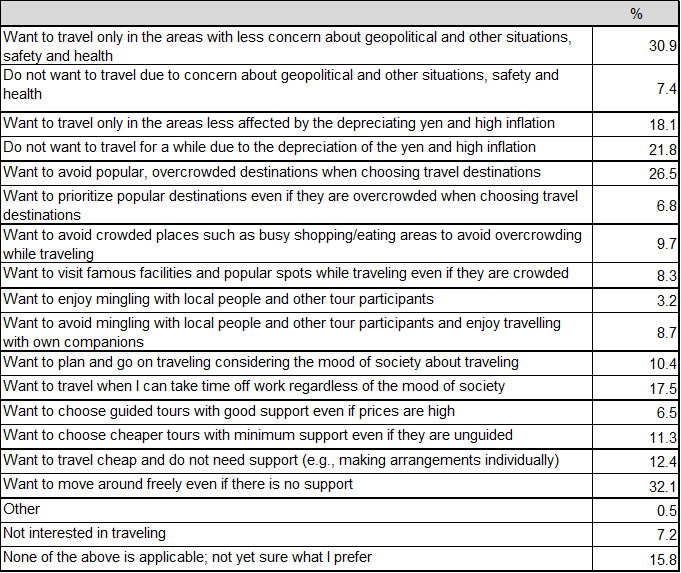

On their view about traveling in the next 12 months, more respondents stated that they would consider geopolitical and other situations, safety, health, and crowds when choosing their destinations with 30.9% of the respondents said that they would want to travel only in the areas with less concern about geopolitical and other situations, safety and health, and 26.5% stated that they would avoid popular, overcrowded destinations. In addition, 21.8% of the respondents did not want to travel for a while due to the depreciation of the Japanese yen and rising inflations. As for travel formats, many respondents preferred free travel with 32.1% wanting to move around freely even if there was no support provided to them and 17.5% wanting to travel when they could take days off work regardless of the mood of society (Figure 5).

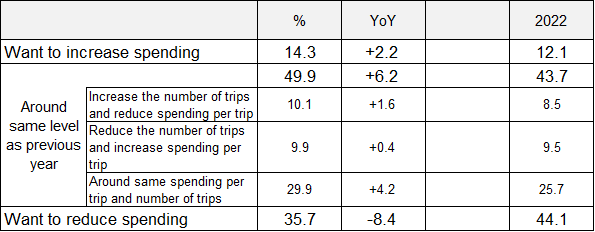

On travel expenditures in the next 12 months, more people plan to increase or maintain their spending compared with a year earlier with a 2.2-pp rise in those wanting to increase spending to 14.3% and an 8.4-pp drop in those wanting to reduce spending to 35.7% (Figure 6).

(Figure 4) Current Living Conditions and Year-end/New Year Period (Multiple answers allowed; N = 10,000)

(Figure 5) Views on Travel in the Next 12 Months (Multiple answers allowed; N = 10,000)

(Figure 6) Travel Expenditure Plan in the Next 12 Months (Single answer; N = 10,000)

<Year-end/New Year Period Travel Forecast>

3. Year-end/new year period travel plans (based on the survey results)

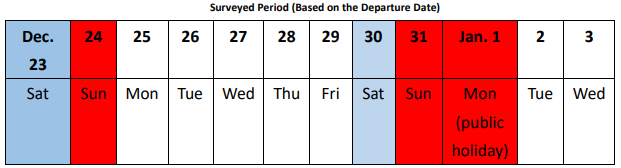

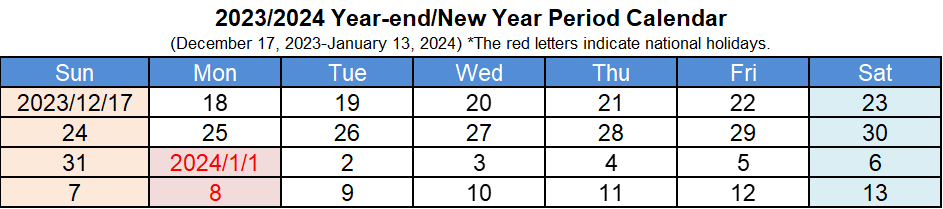

According to the calendar of the 2023/2024 year-end/new year period, the new year holidays from December 30 to January 3 are followed by a long weekend on January 6 to 8. As a result, a certain number of people are expected to travel during the long weekend, avoiding traveling during the new year holiday period. Furthermore, some people may have a long 10-day holiday (from December 30 to January 8), taking time off work on January 4 and 5.

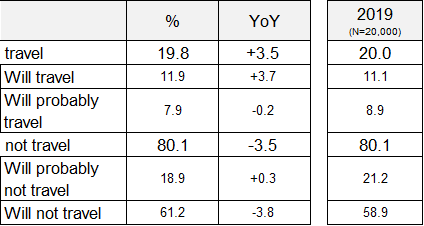

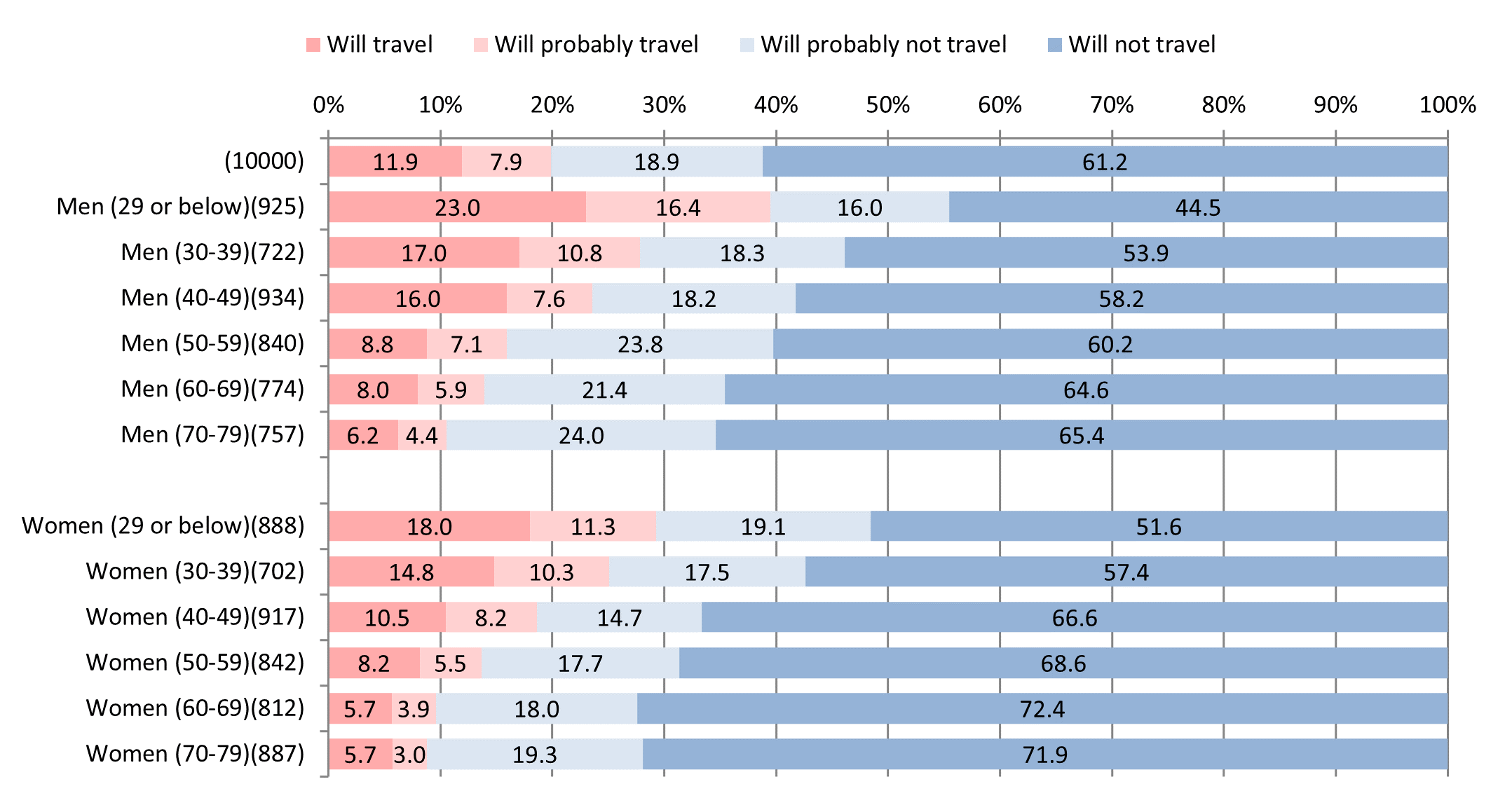

According to the aforementioned survey, the percentage of the respondents who replied they would travel during the 2023/2024 year-end/new year period (total of "Will travel" and "Will probably travel") rose 3.5 pp from a year earlier to 19.8% (Figure 7). Given that this percentage in the same survey conducted in 2019 was 20.0%, it recovered almost to its pre-COVID level. By gender and age, younger generations, both male and female, tend to be keener on travelling. Those who responded that they would travel (total of "Will travel" and "Will probably travel") accounted for 39.4% of male respondents aged 29 or below (up 9.6 pp from a year earlier) and 29.3% of female respondents aged 29 or below (up 4.3 pp from a year earlier). The survey shows that all generations, including seniors who were not keen to travel last year, have become more positive about traveling with 13.9% of male respondents in their 60s (up 2.7 pp from a year earlier), 9.6% of female respondents in their 60s (up 2.4 pp from a year earlier), 10.6% of male respondents in their 70s (up 3.2 pp from a year earlier), and 8.7% of female respondents in their 70s (up 1.1 pp from a year earlier) planning to travel (Figure 8).

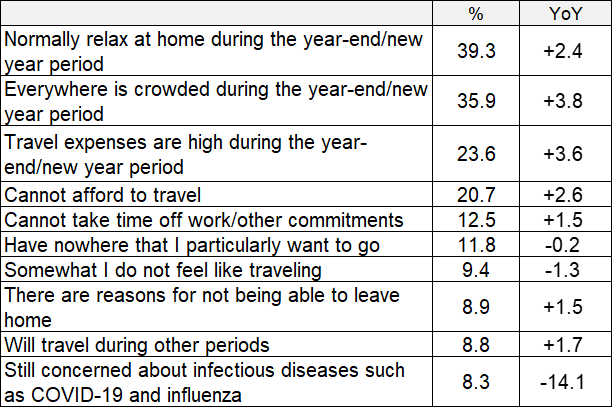

As for reasons for not travelling, the largest number of respondents said they would "Normally relax at home during the year-end/new year period (39.3%)," followed by "Everywhere is crowded during the year-end/new year period (35.9%)." Those who are not traveling for being "Still concerned about infectious diseases such as COVID-19 and influenza" decreased significantly by 14.1 pp from a year earlier to 8.3% (Figure 9).

(Figures 7 & 8) Travel Plans During Year-end/New Year Period (December 23, 2023-January 3, 2024) (Single answer; By gender and age; N = 10,000)

(Figure 9) Reasons for Not Traveling During 2023/24 Year-end/New Year Period (Multiple answers allowed; N = 8,014) (Listing only some of the options provided)

4.2023/24 year-end/new year period travel forecast

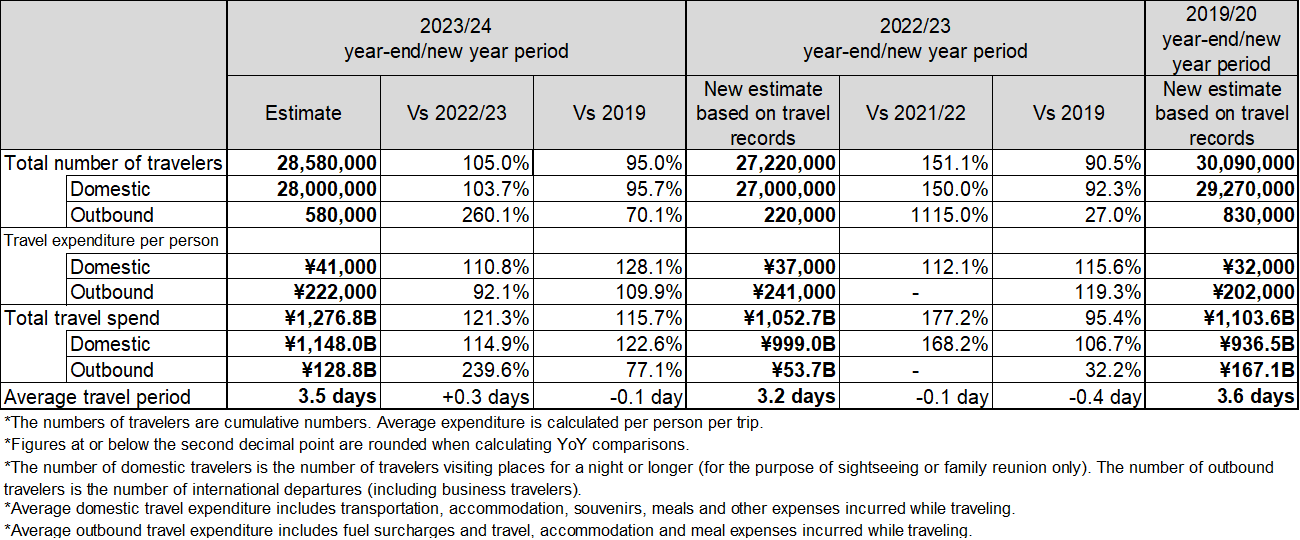

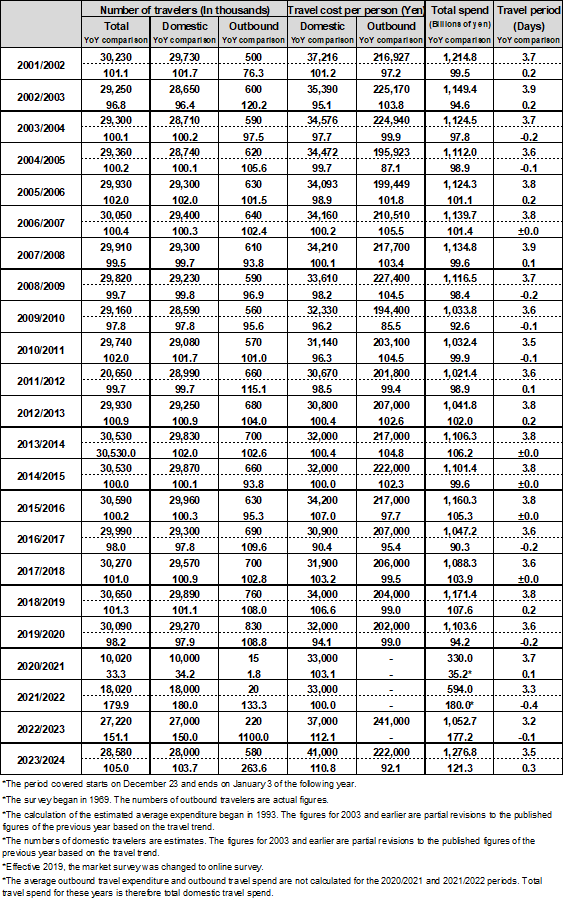

The total number of travelers is estimated at 28,580,000 (105.0% of the same figure a year earlier and 95.0% of 2019).

The number of Japanese domestic travelers is nearing to its 2019 level; travel expenditures are increasing due to inflation and the growing demand for traveling.

The number of outbound travelers is 70.1% of its 2019 level; travel expenditures remain high due to factors such as overseas inflations and the cheaper Japanese yen.

The travel trend of the 2023/24 year-end/new year period (December 23, 2023-January 3, 2024) was calculated based on economic indicators, industry trends, transport company activities, bookings at accommodation facilities, opinion surveys, and other factors. The total number of travelers is estimated at 28,580,000 (105.0% of the same figure a year earlier and 95.0% of 2019) and total travel spend at ¥1,276.8 billion (121.3% of total travel spend a year earlier and 115.7% of 2019).

Of these figures, the number of domestic travelers is estimated at 28 million (103.7% of the same figure a year earlier and 95.7% of 2019), average domestic travel expenditure at ¥41,000 (110.8% of the same figure a year earlier and 128.1% of 2019), and total domestic travel spend at ¥1,148.0 billion (114.9% of the same figure a year earlier and 122.6% of 2019). While consumers' travel appetite has recovered almost to the same level as in 2019, the number of domestic travelers is estimated to be slightly lower than that in 2019 given that the 2023/24 year-end/new year period does not provide a particularly long holiday period, and that a certain number of people may travel on the long weekend on January 6 to 8 instead. The average domestic travel expenditure reached its highest since the start of this survey due to the rising travel-related expenses caused by the growing inflation and demand for traveling, recovery in inbound travel, and labor shortage in service industries.

The number of outbound travelers is estimated at 580,000 (260.1% of the same figure a year earlier and 70.1% of 2019), average outbound travel expenditure at ¥222,000 (92.1% of the same figure a year earlier and 109.9% of 2019), and total outbound travel spend at ¥128.8 billion (239.6% of the same figure a year earlier and 77.1% of 2019). This may partly reflect the long year-end/new year holidays in 2019/2020 when some people had up to nine consecutive holidays. Partly due to inflations overseas, the cheaper Japanese yen, and increases in fuel surcharges between December 2023 and January 2024, the travel period tends to be shorter with more people visiting Asia, which is relatively closer to Japan. On the other hand, a certain number of people are choosing to visit Europe as their first overseas trip in a long while, in addition to Hawaii, which is always a popular destination.

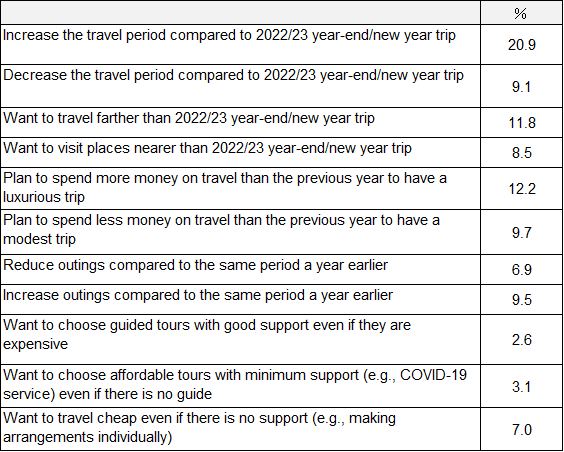

With respect to travel plans for the 2023/24 year-end/new year period, the largest percentage of respondents (20.9%) responded to increase their travel period compared with the same period a year earlier. Their number was significantly higher than those responding to reduce the travel period compared with the same period a year earlier (9.1%). Furthermore, the number of respondents wanting to travel farther than their trip during the 2022/23 year-end/new year period (11.8%) exceeded those wanting to travel to places closer than their trip during the 2022/23 year-end/new year period (8.5%) by 3.3 pp. In addition, the number of respondents planning to spend more money on traveling than the previous year to have more luxurious trips (12.2%) exceeded those planning to spend less money on traveling than the previous year to have modest trips (9.7%) by 2.5 pp. These show the respondents' willingness to travel "longer" and "farther" and "spend more money than a year earlier," probably in reaction to the end of the COVID-19 pandemic (Figure 10).

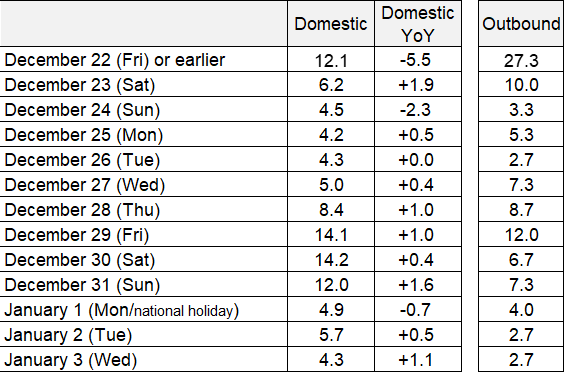

The peak departure dates are December 30 for Japanese domestic travelers and December 22 or earlier for outbound travelers (Figure 11). The departure dates for outbound travelers are earlier because some choose to travel outside the year-end/new year peak period when costs are high with more people travelling and potentially because a certain number of people spend a long time overseas before and after the arrival of the new year.

(Figure 10) 2023/24 Year-end/New Year Travel Plans (Multiple answers allowed; N = 1,930)

(Figure 11) Travel Departure Dates (Single answer; domestic N = 1,780; outbound N = 150)

Specific trends will be discussed in the next and subsequent chapters.

5.2023/24 year-end/new year domestic trips get longer with greater numbers and ranges of travel companions.

Many travel to spend quality time with family, relax, or visit hometown

We analyzed the travel trend of 1,780 respondents who said they would travel in Japan among the respondents of the main survey of the 2023/24 year-end/new year travel survey (1,930 respondents). Compared with two years ago when the COVID-19 pandemic was raging, the travel period began gradually lengthening from last year and travel companions started to expand from close family members to friends and acquaintances. This trend has further accelerated this year, signaling a return to the pre-COVID situation. On the public transport used, the use of railways, ferries/ships, and chartered buses is especially increasing. The detailed survey results are as follows.

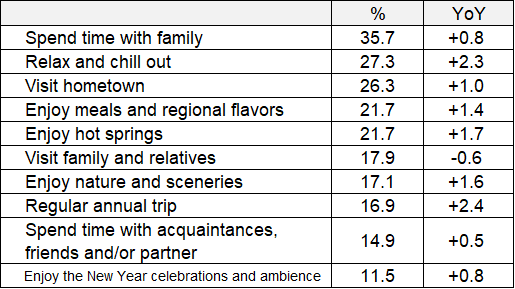

Travel purpose: "Spend time with family" had the largest share at 35.7%. This was followed by "Relax and chill out (27.3%)" and "Visit hometown (26.3%)." With respect to the rate of increase from a year earlier, the ratio of respondents who chose as the reasons for travel "Regular annual trip (16.9%)" and "Relax and chill out (27.3%)" rose 2.4 pp and 2.3 pp, respectively (Figure 12).

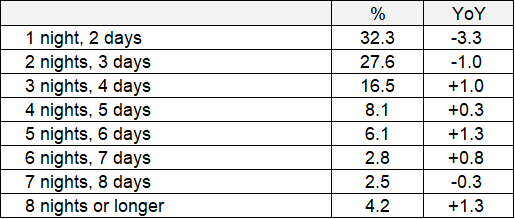

Travel period: Overall, the ratio of respondents who were going to have a one-night, two-day trip (32.3%) was largest, but it fell by 3.3 pp from a year earlier. The ratio of those going on a two-night, three-day trip (27.6%) also fell by 1.0 pp. Meanwhile, the ratios of respondents spending three nights, four days to six nights, seven days all rose from a year earlier, showing a move away from the trend of going on shorter trips that continued during the COVID-19 pandemic (Figure 13).

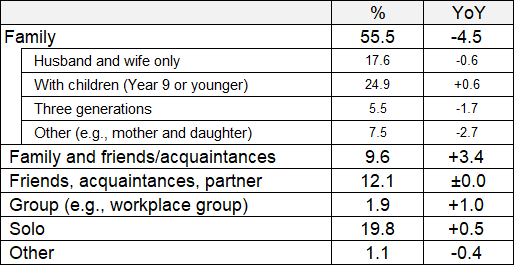

Travel companions: The ratio of respondents going on a family trip with children (Year 9 or younger) was largest at 24.9%, followed by "Solo trip (19.8%)" and "Husband and wife only (17.6%)." Looking at the rate of increase from a year earlier, the ratio of respondents travelling with "Family and friends/acquaintances" rose 3.4 pp to 9.6% and those travelling in a "Group (e.g., workplace group)" increased 1.0 pp to 1.9%. There is a tendency of the expansion in the range of travel companions from family or solo trips, which increased during the COVID-19 pandemic (Figure 14).

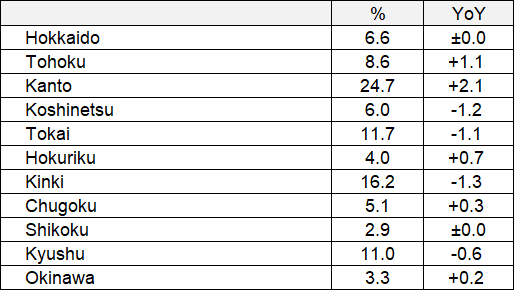

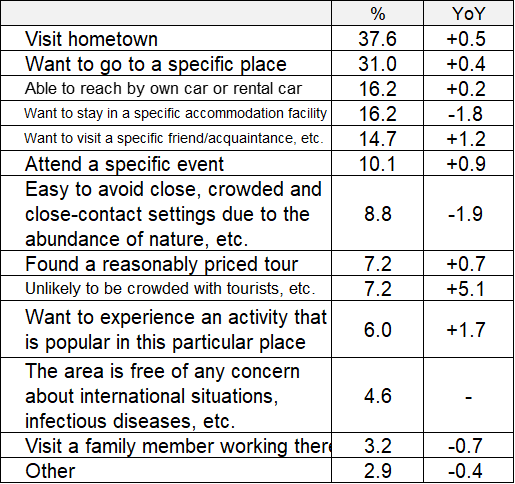

Travel destinations: "Kanto" was the most popular destination with 24.7% of respondents travelling there, followed by "Kinki (16.2%)" and "Tokai (11.7%)" (Figure 15). As for the reasons for choosing these destinations, the largest percentage of respondents said they "Visit hometown (37.6%)," followed by "Want to go to a specific place (31.0%)" and "Able to reach by own car or rental car (16.2%)" (Figure 16).

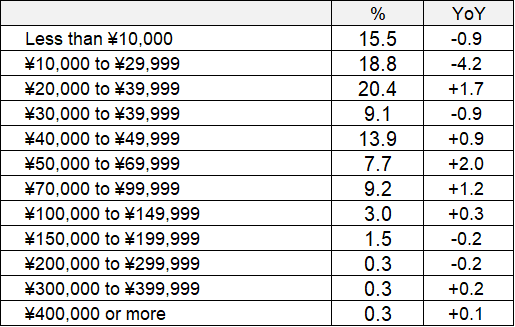

Travel expenditure per person: Overall, the ratio of respondents spending "¥20,000 to ¥29,999" is largest at 20.4%, rising 1.7 pp from a year earlier, followed by those spending "¥10,000 to ¥19,999" at 18.8%, which fell by 4.2 pp from a year earlier. The combined ratio of those spending ¥40,000 or more rose by 4.3 pp from a year earlier. Overall, travel expenditures are rising (Figure 17).

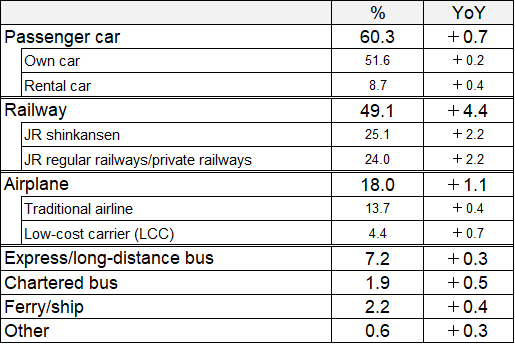

Transport: The ratio of respondents using "Own car" was largest at 51.6%, followed by "JR shinkansen" at 25.1% and "JR regular railways/private railways" at 24.0%. There was an increase in the use of all modes of transport compared with a year earlier. This indicates the use of multiple types of transport systems due to the lengthening of travel periods (Figure 18).

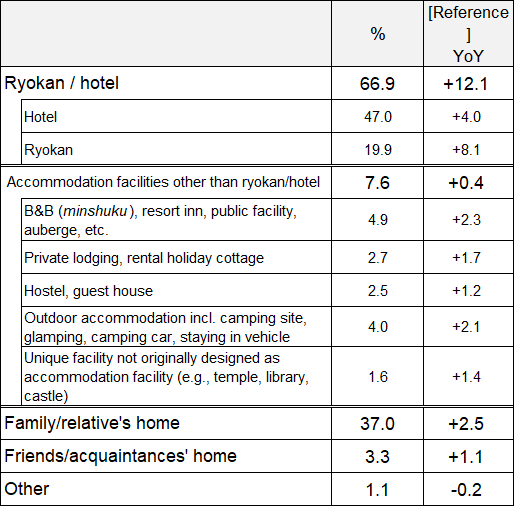

Accommodation facilities: The ratio of respondents staying in "Hotels" was highest at 47.0%, followed by "Family/relative's home" at 37.0% and "Ryokans" at 19.9% (Figure 19).

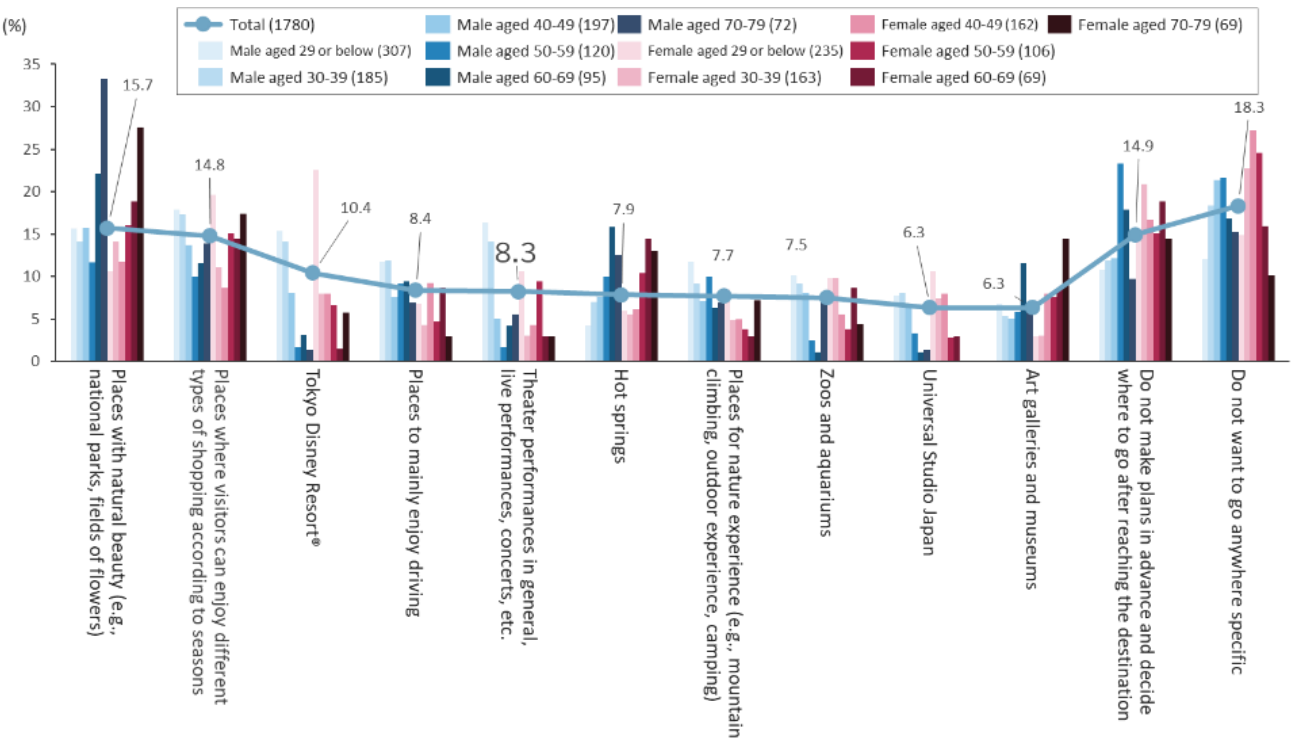

As for the places of interest, the largest percentage of respondents chose "Places with natural beauty (e.g., national parks and fields of flowers) (15.7%)," followed by "Places where visitors can enjoy different types of shopping according to seasons (14.8%)." By gender and age, high proportions of both male and female respondents in their 70s chose "Places with natural beauty (e.g., national parks and fields of flowers)" and "Art galleries and museums," while high proportions of both male and female respondents aged 29 or below chose "Places where visitors can enjoy different types of shopping according to seasons," "Tokyo Disney Resort®," "Theater performances in general, live performances, concerts, etc.," and "Universal Studio Japan" (Figure 20).

The bookings of accommodation/domestic special products of JTB grew 15% from a year earlier (as of December 4) thanks to the recovery in the appetite for traveling. The bookings are especially strong for products that are bound for Tokyo including Tokyo Disney Resort® and products bound for Kansai including Universal Studio Japan, showing the continuously strong demand for theme parks that offer seasonal events. The bookings for long distance products bound for Hokkaido, Kyushu, and so on are also strong.

(Figure 12) Travel Purpose (Single answer; N = 1,780) (Excerpts of the options)

(Figure 13) Travel Period (Single answer; N = 1,780)

(Figure 14) Travel Companions (Single answer; N = 1,780)

(Figure 15) Travel Destinations (Single answer; N= 1,780)

(Figure 16) Reasons for Choosing Destinations (Single answer; N = 1,780)

(Figure 17) Travel Expenditure per Person (Single answer; N = 1,780)

(Figure 18) Transport (Multiple answers allowed; N = 1,780)

(Figure 19) Accommodation Facilities (Multiple answers allowed; N = 1,780)

(Figure 20) Places of Interest for 2023/24 Year-end/New Year Trips (By Gender/Age) (Multiple answers allowed; N = 1,780)

6. International travel is yet to make full recovery despite positive factors such as recovery in international passenger flights.

Compared with 2019, the travel period is slightly shorter, although the difference is small; travel expenditures are polarized; Hawaii, South Korea, and Southeast Asia are popular destinations.

Despite the anticipated, full recovery in international travel following the termination of Japan's border control measures on April 29, 2023, the number of Japanese outbound travelers is yet to make full recovery. With the rapid return of international regular passenger flights departing from and arriving in Japan, some survey results have shown that, in the summer of 2023, inbound and outbound flights to and from Japan recovered to about 70% of their pre-COVID levels. They are expected to further grow in the winter of 2023 including the 2023/24 year-end/new year period.

Meanwhile, increases in flights and seating capacity may be in response to the robust demand from inbound tourists to Japan. Furthermore, the increased supply is slow to result in the higher number of outbound Japanese travelers as the Japanese citizens face the cheaper Japanese yen, inflations overseas, and increases in fuel surcharges between December 2023 and January 2024.

Given these situations, the number of outbound tourists during the 2023/24 year-end/new year period is estimated at around 580,000. This represents 260.1% of the same figure a year earlier and 70.1% of 2019.

Of the 1,930 respondents participating in this survey, 150 people said that they had travelled overseas during the summer holidays in 2023 (7.8%), an increase of 5.7 pp from a year earlier. For reference, the said ratio was 8.4% in 2019.

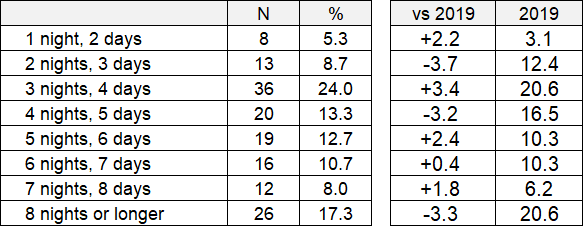

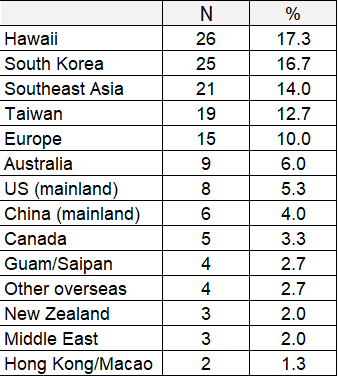

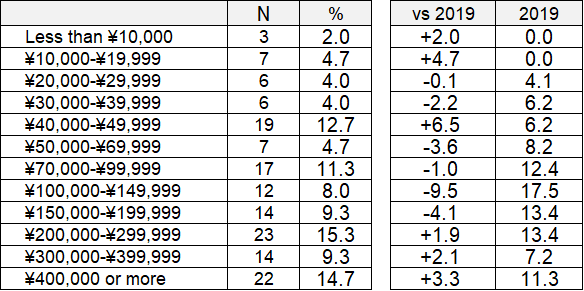

The ratio of respondents travelling for "3 nights, 4 days" was largest at 24.0%, followed by those travelling for "8 nights or longer (17.3%)," "4 nights, 5 days (13.3%)," and "5 nights, 6 days (12.7%)." Compared with the same period in 2019, the ratio of respondents travelling for "3 nights, 4 days" or shorter rose 1.9 pp, while those travelling for "6 nights, 7 days" or longer fell 1.1 pp. The popular destinations are Hawaii (17.3%), South Korea (16.7%), and Southeast Asia (14.0%), in the descending order of popularity. As for travel expenditure, the ratio of respondents spending "¥200,000 to ¥299,999" was largest at 15.3%, followed by those spending "¥400,000 or more (14.7%)" and "¥40,000 to ¥49,999 (12.7%)." In comparison with the same period in 2019, the combined ratio of respondents spending less than ¥50,000 increased 10.9 pp, while the combined ratio of those spending ¥200,000 or more also rose 7.3 pp. Among those traveling internationally during the 2023/24 year-end/new year period, the ratio of those who will go on a long trip rose close to its pre-COVID level. Many people also travel to distant destinations such as Hawaii and Europe in addition to nearer destinations such as South Korea, Southeast Asia, and Taiwan. This led to the polarization of travel expenditures (Figures 21, 22 and 23). The bookings of JTB's outbound special products represent 640% of the bookings made a year earlier (as of December 4). With the polarizing trend of the travel period and expenditures, popular destinations include Hawaii and Australia for those traveling far and Guam, Taiwan, and South Korea for those traveling to nearer destinations.

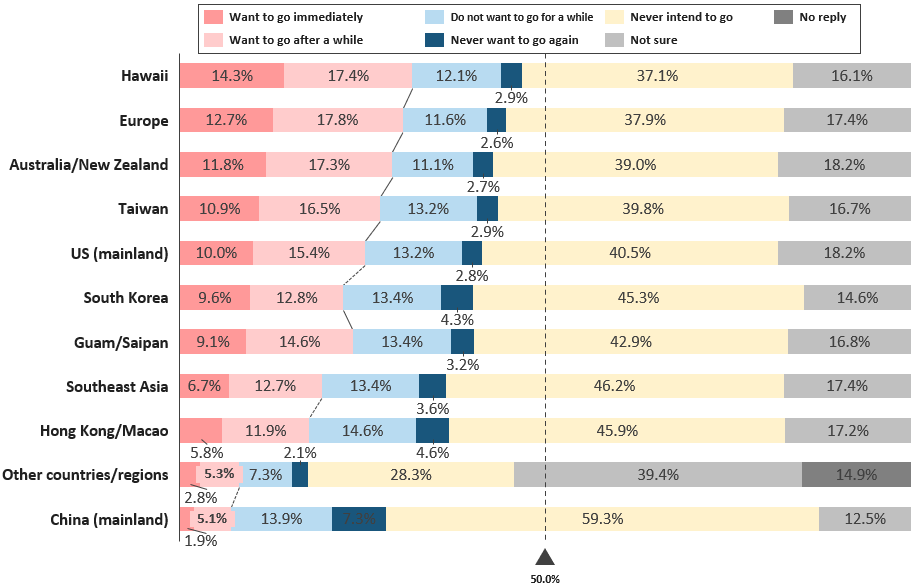

The survey also questioned future outbound travel intensions of the participants of the preliminary survey who were not planning to travel during the 2023/24 year-end/new year period. In terms of the timing of travel by destination, the ratio of those who "Want to go immediately" was highest for "Hawaii" at 14.3%, followed by 12.7% for Europe and 11.8% for Australia/New Zealand. In East Asia, Taiwan came first at 10.9%, followed by South Korea at 9.6%, showing a clear trend of divisions between distant and close destinations (Figure 24).

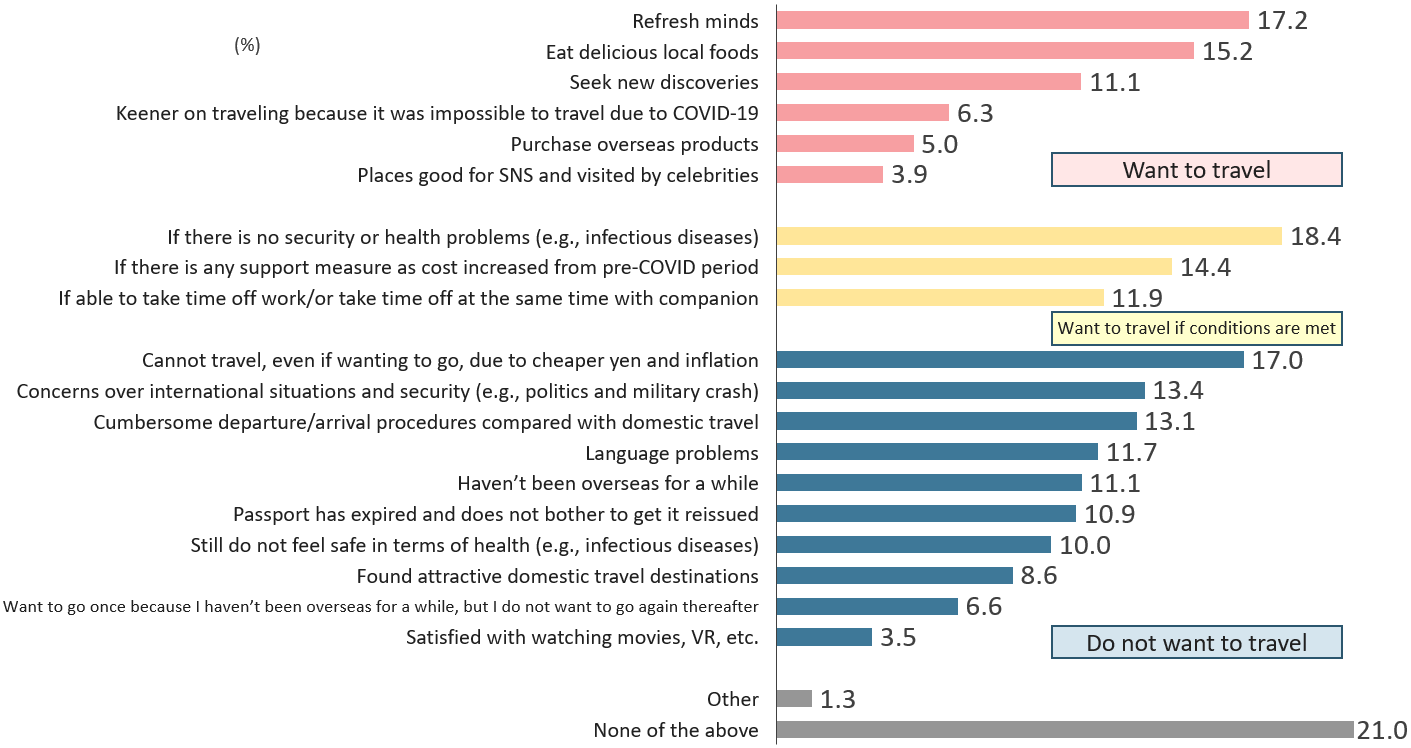

In addition, when asked about the current thought on international travel, in terms of positive responses, the respondents showed a tendency to prioritize the long-established purposes of travel such as to "Refresh minds (17.2%)" and "Eat delicious local foods (15.2%)". On the other hand, the respondents also expressed negative opinions about international travel from safety or economic aspects such as wanting to travel "If there is no security or health problems (e.g., infectious diseases) (18.4%) ," "Cannot travel, even if wanting to go, due to cheaper yen and inflation(17.0%)," and "Concerns over international situations and security (e.g., politics and military crash) (13.4%)". It is hoped that a safe and more affordable travel environment be created (Figure 25).

(Figure 21) Travel Period (Outbound) (Single answer; 2023 N = 150; 2019 N = 97)

(Figure 22) Destinations (Outbound) (Single answer; N = 150)

(Figure 23) Travel Expenditure per Person (Outbound) (Single answer; 2023 N = 150; 2019 N = 97)

(Figure 24) Future International Travel Intensions by Destination (Single answer; N = 10,000)

(Figure 25) Current International Travel Intensions (Multiple answers allowed; N = 10,000)

(Figure 26) Estimated Number of Travelers/Travel Expenditure for Year-end/New Year Period

JTB Corp. Branding & Communication Team (Public Relations)

Phone: +81 3 5796 5833